Why Is Buying a Home Not as Great as It Used to Be?

Homeownership has long been a cornerstone of the American Dream, but in 2025, many are questioning whether buying a home is not as great as it once was. Rising costs, economic shifts, and changing lifestyles have made purchasing a home less appealing for some. In this article, we’ll explore why homeownership has lost some of its luster, backed by current market trends, and offer alternatives for those rethinking their housing plans.

Rising Costs Make Homeownership Less Affordable

One of the biggest reasons buying a home is not as great today is the skyrocketing cost of housing. From home prices to interest rates, financial barriers are higher than ever.

Soaring Home Prices

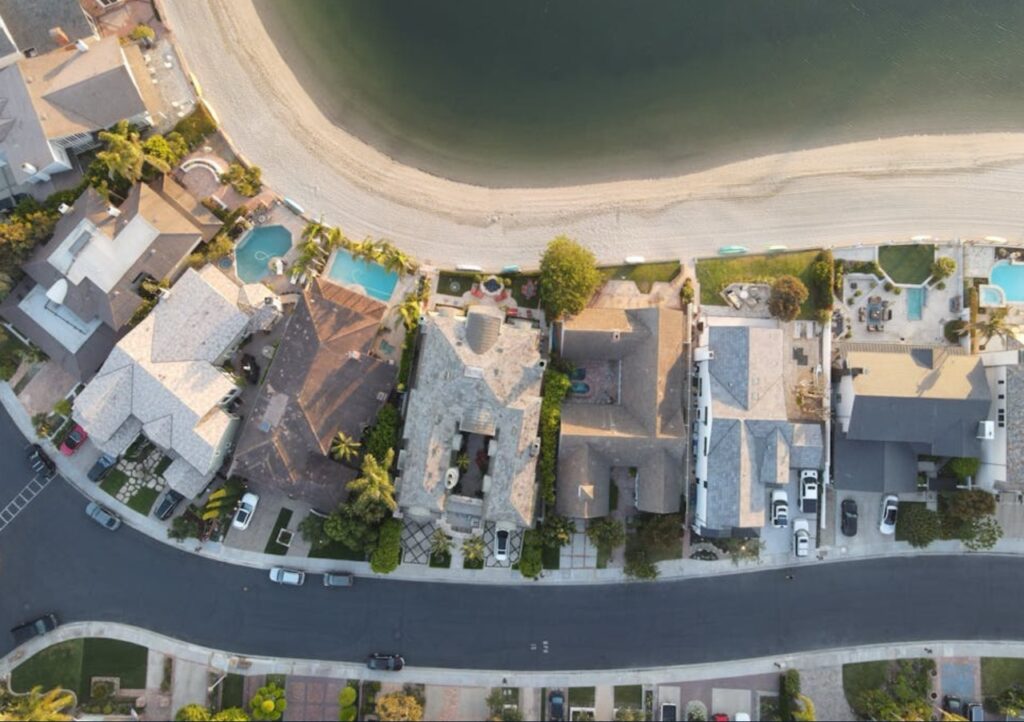

In 2025, median home prices in the U.S. hover around $412,000, with coastal markets like California exceeding $800,000. According to Redfin, home prices have outpaced wage growth, making it harder for first-time buyers to afford a down payment. This affordability gap leaves many feeling that homeownership is out of reach compared to past decades when homes were more reasonably priced relative to income.

Higher Interest Rates

Mortgage rates in 2025 are projected to range between 6-7%, up from the historic lows of 2-3% seen in 2020-2021. Higher rates increase monthly payments, adding thousands to the cost of a loan over time. For example, a $400,000 mortgage at 6.5% costs significantly more per month than at 3%, discouraging buyers who remember cheaper borrowing conditions.

Market Challenges and Uncertainty

Beyond costs, the housing market itself presents hurdles that make buying a home not as great as it used to be. Competitive markets and economic factors add complexity to the process.

Low Inventory and Bidding Wars

A persistent shortage of homes, especially in desirable areas, drives intense competition. Bidding wars push prices above asking, forcing buyers to stretch budgets or compromise on their dream home. Web searches indicate that 67% of Americans in 2024 felt the housing market was unaffordable, a sentiment echoed in 2025 as inventory remains tight.

Economic and Job Market Instability

Uncertainty in the job market, coupled with inflation, makes buyers hesitant to commit to long-term mortgages. Posts on X highlight fears of overpaying in a market that could cool, leaving homeowners underwater if prices drop. This risk feels more pronounced than in previous eras of stable growth.

Shifting Lifestyle Preferences

Changing priorities among younger generations also contribute to why buying a home is not as great as it once was. Flexibility and financial freedom are taking precedence over traditional homeownership.

Renting Offers More Flexibility

Millennials and Gen Z value mobility, especially with remote work enabling location independence. Renting allows them to relocate for jobs or lifestyle changes without the burden of selling a home. In 2025, renting is often seen as a smarter choice in high-cost cities where monthly mortgage payments far exceed rent.

Maintenance and Hidden Costs

Owning a home comes with ongoing expenses—property taxes, insurance, and maintenance—that can strain budgets. Web sources note that homeowners spend 1-4% of a home’s value annually on upkeep. For many, these costs outweigh the benefits of building equity, especially when compared to the simplicity of renting.

Is Homeownership Still Worth It?

While buying a home is not as great for everyone, it still has merits for some. Long-term equity, stability, and personalization are draws for those who can afford it. However, the financial and emotional toll of entering today’s market makes it less universally appealing.

Alternatives to Buying a Home

If homeownership feels out of reach, consider these options:

- Renting Strategically: Choose affordable rentals in up-and-coming areas to save for a future purchase.

- Co-Buying: Partner with friends or family to split costs, a growing trend in 2025.

- First-Time Buyer Programs: Explore FHA loans or state grants to reduce down payment barriers.

- Investing Elsewhere: Build wealth through stocks or real estate investment trusts (REITs) without the hassle of homeownership.

Tips for Navigating the 2025 Housing Market

If you’re still set on buying, here’s how to make it work despite the challenges:

Shop in Emerging Markets

Look beyond pricey urban centers to suburbs or secondary cities like Raleigh or Boise, where prices are more manageable and appreciation potential is strong.

Get Pre-Approved

A mortgage pre-approval strengthens your offer in competitive markets and clarifies your budget. Work with a lender to lock in the best rate possible.

Plan for Long-Term Ownership

Given high upfront costs, aim to stay in your home for at least 5-10 years to build equity and offset closing costs. This approach mitigates the risk of market fluctuations.

Final Thoughts

So, why is buying a home not as great as it used to be? Soaring prices, higher interest rates, market competition, and shifting priorities have dimmed the appeal of homeownership for many in 2025. While it remains a solid investment for some, others find renting or alternative investments better suit their goals. Evaluate your finances, lifestyle, and local market before deciding, and consider consulting a financial advisor to weigh your options.

Ready to explore your path? Research local market trends, explore renting, or connect with a real estate professional to make an informed choice in 2025.